The IRS Confronts a Delicate Balancing Act: Targeting Small Business Non-Compliance in the Tax Gap Battle

In the ongoing saga of addressing the tax gap in the United States, the role of small businesses has become a focal point of discussion. This revelation, though seemingly straightforward, has emerged as a sensitive and contentious issue within the political landscape. The IRS, in its continuous quest to close the tax gap, has asserted that small businesses are not their primary enforcement priority. Even with additional funding allocated in the IRA 2022 initiative, the IRS has maintained that it will not substantially increase its audit presence on small businesses compared to historical rates. However, this stance raises the critical question of whether overlooking small business non-compliance is a feasible strategy if the IRS intends to make a meaningful impact on the tax gap.

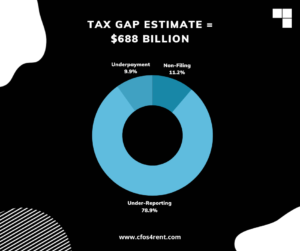

The latest estimates for t he 2021 tax gap affirm the persistent significance of small business non-compliance. Analysis by the Committee for a Responsible Federal Budget, which examines past tax gap studies, illustrates that over half of the underreporting tax gap can be attributed to small businesses. The data from the 2021 projections reinforces this conclusion and emphasizes the pressing need to address non-compliance among small businesses.

he 2021 tax gap affirm the persistent significance of small business non-compliance. Analysis by the Committee for a Responsible Federal Budget, which examines past tax gap studies, illustrates that over half of the underreporting tax gap can be attributed to small businesses. The data from the 2021 projections reinforces this conclusion and emphasizes the pressing need to address non-compliance among small businesses.

A deep dive into the underreporting tax gap estimates for 2021 reveals a substantial portion linked to small business activities. Out of the projected $542 billion in underreporting for that year, a staggering $271 billion, or 50%, pertains to small business enterprises. This breakdown includes:

- Individual Business Income Tax: $182 billion.

- Small Corporation Income Tax: $21 billion.

- Self-Employment Tax: $68 billion.

It is important to note that the actual small-business tax gap may be even greater than what the IRS projects. Limited data availability on S corporation and partnership non-compliance complicates the overall assessment. Many S corporations, which constitute the majority of small businesses, are often single-owner entities that grapple with issues related to payment, non-filing, and, notably, underreporting.

As the IRS grapples with the complexities of addressing the tax gap, it finds itself in a delicate balancing act. While small business non-compliance is a clear and substantial contributor to the tax gap, the agency must navigate the intricacies of enforcement priorities, resource allocation, and political sensitivities. Finding an effective and equitable solution to this multifaceted challenge will be pivotal in the IRS’s quest to bridge the tax gap and ensure tax revenue is collected in accordance with the law.